50-Year Mortgage Explained: Pros, Cons, Tax Savings & Comparison to 15, 30, 40-Year Loans

The 50-year mortgage is a bold proposal aimed at lowering monthly payments, but it comes with significant long-term costs and risks.

What Is a 50-Year Mortgage?

A 50-year mortgage is a fixed-rate home loan stretched across five decades—600 monthly payments compared to the 360 payments of a traditional 30-year mortgage. The idea was recently floated by President Donald Trump and Federal Housing Finance Agency Director Bill Pulte as a way to address the housing affordability crisis.

Why It’s Being Proposed

- Housing affordability crisis: Home prices remain high, interest rates elevated, and inventory tight.

- Lower monthly payments: By spreading costs over 50 years, borrowers could save $2,000 annually compared to a 30-year loan.

- Access to homeownership: Supporters argue it could help younger buyers and those struggling to qualify for traditional loans.

⚠️ Risks and Criticisms

- Equity builds slowly: Most payments in the first decade go toward interest, leaving homeowners vulnerable if prices fall.

- Higher lifetime costs: Borrowers would pay hundreds of thousands more in interest over the life of the loan.

- Default risk: With limited equity, homeowners face greater risk of foreclosure during economic downturns.

- Banks may raise rates: Lenders could offset risk by charging higher interest, erasing much of the monthly savings.

- Doesn’t fix supply issues: Critics argue it’s a band-aid solution that doesn’t address the root problem—too few homes on the market.

Example: 30-Year vs. 50-Year

| Loan Term | Monthly Payment (Approx.) | Total Interest Paid | Equity Growth |

|---|---|---|---|

| 30-Year | Higher | Lower | Faster |

| 50-Year | Lower | Much Higher | Slower |

Sources:

What It Means for Buyers

The 50-year mortgage could make homeownership more accessible in the short term, especially for first-time buyers squeezed by high prices. But the trade-off is long-term debt, slower wealth-building, and higher overall costs. For many, it may feel like renting from the bank for life rather than owning a home outright.

️ Key Perspectives on the 50-Year Mortgage

| Person / Group | Position / Statement | Tone / Implication |

|---|---|---|

| Donald Trump (President) | Floated the idea on Truth Social, calling it a way to lower monthly payments and help young people buy homes | Supportive, framing it as part of the “American Dream” |

| Bill Pulte (FHFA Director) | Called it a “complete game changer” and said the agency is working on it | Strongly supportive, presenting it as a bold affordability solution |

| White House Officials (anonymous sources) | Some said Trump was lukewarm and only announced it to quiet Pulte; others confirmed discussions of 40- and 50-year terms | Mixed, with internal disagreement and frustration over rollout |

| Conservative Allies of Trump | Expressed skepticism, warning it could benefit banks more than buyers and increase total interest costs | Critical, worried about long-term debt burden |

| Housing Industry Experts | Warn that savings would be minimal, equity would build very slowly, and borrowers would pay hundreds of thousands more in interest | Cautious to negative, highlighting risks over benefits |

| Public Reaction (online commentators) | Many criticized the idea as increasing debt levels and failing to fix supply issues | Negative, viewing it as a band-aid solution |

Takeaway

The 50-year mortgage is being promoted by Trump and Bill Pulte as a way to expand access to homeownership, especially for younger buyers. But critics—including some within Trump’s own circle—argue it’s financially risky, benefits banks more than families, and doesn’t solve the housing supply crunch.

Loan Comparison: $300,000 Mortgage at 6% Interest

| Loan Term | Monthly Payment | Total Paid Over Life | Total Interest Paid | Equity Growth Speed |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $455,000 | ≈ $155,000 | Very fast – builds equity quickly |

| 30-Year | ≈ $1,800 | ≈ $648,000 | ≈ $348,000 | Moderate – standard equity growth |

| 40-Year | ≈ $1,650 | ≈ $792,000 | ≈ $492,000 | Slow – equity builds much later |

| 50-Year | ≈ $1,580 | ≈ $948,000 | ≈ $648,000 | Very slow – equity builds extremely late |

Key Takeaways

- Monthly Relief: The 50-year loan cuts payments by about $950 compared to a 15-year loan.

- Long-Term Cost: That relief comes at a steep price—interest nearly quadruples compared to a 15-year loan.

- Equity Risk: With 40- and 50-year loans, homeowners spend decades paying mostly interest, leaving them vulnerable if housing prices dip.

- Wealth Building: Shorter terms (15-year) are far better for building equity and reducing lifetime debt.

Mortgage Term Comparison on a $300,000 Loan (6% Interest)

| Loan Term | Monthly Payment | Total Interest Paid | Pros | Cons |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $155,000 | – Builds equity fastest – Lowest total interest – Own home sooner |

– Highest monthly payment – Harder to qualify due to income requirements |

| 30-Year | ≈ $1,800 | ≈ $348,000 | – Standard option, widely available – Balanced monthly payment – Easier to qualify |

– Pays more than double the interest of 15-year – Slower equity growth |

| 40-Year | ≈ $1,650 | ≈ $492,000 | – Lower monthly payment than 30-year – Expands affordability for buyers |

– Much higher lifetime interest – Very slow equity buildup – Limited availability |

| 50-Year | ≈ $1,580 | ≈ $648,000 | – Lowest monthly payment – Makes homeownership accessible for more buyers – Short-term affordability relief |

– Enormous interest burden – Equity builds extremely slowly – Riskier if housing prices fall – May feel like “renting from the bank” |

Big Picture

- Shorter terms (15-year) → Best for wealth-building, lowest cost, but hardest to afford monthly.

- Middle ground (30-year) → Most common, balances affordability and long-term cost.

- Extended terms (40- and 50-year) → Lower monthly payments, but huge long-term debt and slow equity growth.

Possible Tax Savings with a 50-Year Mortgage

One of the few potential upsides of a longer mortgage term is the mortgage interest deduction available to many U.S. taxpayers. Here’s how it could play out:

How It Works

- Mortgage Interest Deduction: Homeowners who itemize deductions can subtract mortgage interest payments from taxable income.

- Longer Terms = More Interest: A 50-year loan front-loads interest payments, meaning borrowers pay interest for decades before significantly reducing principal.

- Tax Benefit: Higher interest payments in the early years could lead to larger deductions, lowering taxable income.

✅ Potential Advantages

- Bigger deductions in early years: Since most of the payment is interest, itemizers may see more tax savings initially.

- Extended deduction period: With interest stretched over 50 years, homeowners could benefit from deductions for a much longer time.

- Helps cash flow: Lower monthly payments plus tax savings could ease financial strain for some households.

⚠️ Limitations

- Standard deduction hurdle: Many taxpayers don’t itemize because the standard deduction is higher; in those cases, the mortgage interest deduction provides no benefit.

- Long-term cost outweighs savings: The extra interest paid over 50 years far exceeds any tax benefit.

- Policy uncertainty: Tax laws can change, so relying on deductions decades into the future is risky.

- Equity trade-off: Even with tax savings, homeowners build equity very slowly, limiting wealth creation.

Bottom Line

While the 50-year mortgage could generate larger and longer-lasting tax deductions, the overall financial burden is still much heavier than shorter loans. Tax savings may soften the blow, but they don’t erase the fact that borrowers pay hundreds of thousands more in interest.

Perfect — let’s illustrate how tax savings from mortgage interest deductions could look across different loan terms for a $300,000 loan at 6% interest.

⚠️ Note: These are simplified estimates assuming the borrower itemizes deductions and is in a 22% federal tax bracket. Actual savings depend on tax law changes, income, and whether the standard deduction is higher than itemized deductions.

Estimated Tax Savings by Loan Term (First-Year Interest Deduction)

| Loan Term | Monthly Payment | First-Year Interest Paid | Estimated Tax Savings (22% Bracket) | Long-Term Deduction Pattern |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $17,800 | ≈ $3,900 | Declines quickly as principal is paid down |

| 30-Year | ≈ $1,800 | ≈ $17,950 | ≈ $3,950 | Moderate decline, deductions last ~20–25 years |

| 40-Year | ≈ $1,650 | ≈ $17,980 | ≈ $3,955 | Very slow decline, deductions extend ~30+ years |

| 50-Year | ≈ $1,580 | ≈ $17,990 | ≈ $3,958 | Extremely slow decline, deductions extend nearly lifetime |

Key Insights

- First-year savings are nearly identical across all terms because interest dominates early payments.

- Shorter loans (15-year): Tax savings taper off quickly as principal is paid faster.

- Longer loans (40- and 50-year): Tax deductions last decades longer, but this comes at the cost of hundreds of thousands more in interest overall.

- Net effect: The tax benefit is real but doesn’t outweigh the massive extra interest paid on ultra-long loans.

This table shows why the 50-year mortgage might look appealing for tax deductions in the short run, but the long-term financial trade-off is steep.

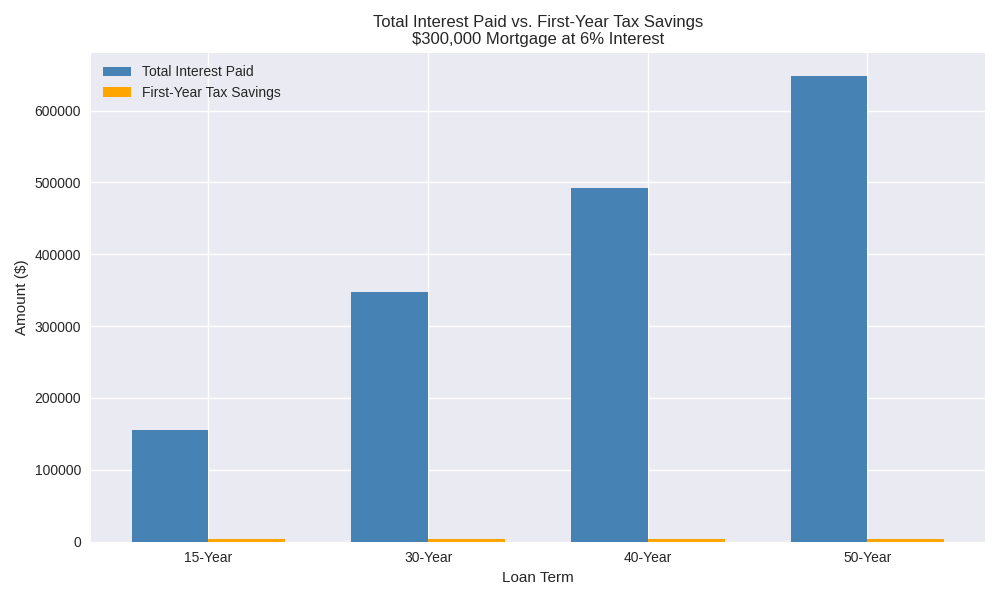

What the Chart Shows

- Blue bars = Total interest paid over the life of the loan

- Orange bars = First-year tax savings from mortgage interest deduction (22% bracket)

- Key Insight: While tax savings are nearly identical across terms (~$3,900 in year one), the interest burden skyrockets as the loan term lengthens.

Breakdown

- 15-Year Loan: ~$155k interest vs. ~$3.9k tax savings → best for wealth-building.

- 30-Year Loan: ~$348k interest vs. ~$3.95k tax savings → balanced but costly.

- 40-Year Loan: ~$492k interest vs. ~$3.96k tax savings → affordability trade-off.

- 50-Year Loan: ~$648k interest vs. ~$3.96k tax savings → tax benefit dwarfed by debt.

Takeaway

The chart makes it clear: tax deductions don’t scale with the exploding interest costs. The 50-year mortgage offers extended deductions, but the long-term debt burden far outweighs the benefit.