rsteelesr79

What Does Selling A House As-Is Mean

What Does Selling a House As-Is Mean? | CanSellYourHouse.com

If you are searching for what does selling a house as-is mean?, you probably want more than a generic real estate explanation. You want to know what your realistic options are, what can slow the sale down, how to protect your net proceeds, and how to move forward without unnecessary repairs, showings, or pressure. This guide is written for homeowners in Virginia who want a practical, WordPress-ready explanation of the selling process.

Need a simple option? CanSellYourHouse.com can review the property, explain the numbers, and give you a no-obligation cash offer so you can compare your choices clearly.

What What Does Selling A House As-Is Mean? Really Means

The original topic behind this page is simple: homeowners need a clear path when the normal selling process feels too slow, too expensive, or too uncertain. In practical terms, If you’re wondering what it means to sell house as is , you’re not alone. Selling a house “as is” means selling your property in its current condition without making any repairs or improvements before the sale. This option can save you time, money, and stress, especially if your home needs repairs or if you want to sell quickly. Understanding the Concept: What Does Selling a House As Is Mean?. The better approach is to compare each option by timeline, risk, required repairs, and final net proceeds.

For most sellers, the phrase what does selling a house as-is mean? does not mean accepting the first number offered or ignoring the home’s value. It means choosing a sale strategy that matches the condition of the property and the seller’s deadline. A fully updated house with no title issues may do well on the open market. A property with repairs, tenants, liens, inherited ownership, foreclosure pressure, or a seller who has already moved may need a different plan.

Common Reasons Homeowners in Virginia Want a Faster Sale

- Speed:*Selling as-is often results in a faster sale because buyers know there won’t be delays due to repair negotiations.

- Cost Savings:*You avoid upfront repair expenses, inspection costs, and renovation hassles.

- Simplicity:*There’s less paperwork and fewer contingencies, making the process straightforward.

- Ideal for Problem Properties:*Homes with significant damage, outdated features, or title issues are often best sold as-is.

- Fair Cash Offers*– We provide transparent, no-obligation cash offers based on your home’s current condition.

- Local Expertise*– Our team understands Richmond’s real estate market and can guide you every step of the way.

Virginia sellers should remember that local custom, title work, taxes, payoff timing, and settlement details can affect the final net number. A good selling plan starts by naming the real problem. A homeowner who needs to avoid a looming deadline needs a different strategy than a homeowner who simply wants the highest possible list price. Once the goal is clear, it becomes easier to decide between a traditional listing, a direct cash sale, a short preparation period, or holding the property longer.

Your Main Selling Options

1. List the House With an Agent

A traditional listing can expose the property to retail buyers and may produce the highest contract price when the home is clean, financeable, easy to show, and priced correctly. The tradeoff is that the seller usually deals with preparation, photographs, showings, inspection negotiations, appraisal risk, buyer financing, and a closing timeline that depends on the buyer’s lender. Sellers should compare the likely list-price outcome against commissions, repair credits, mortgage payments, insurance, taxes, utilities, and the time spent waiting.

2. Sell Directly to a Cash Buyer

A direct cash sale is designed for convenience and certainty. The buyer reviews the home, makes an offer based on its present condition, and closes through a title or settlement company. The seller can often avoid repairs, deep cleaning, staging, open houses, and repeated negotiation. The offer may be lower than a perfect retail list price, but the seller should compare it to the realistic net after all traditional selling costs.

3. Make Repairs Before Selling

Repairs can help when the work is affordable, the scope is clear, and the finished improvements will increase buyer confidence. Repairs can also become a trap when contractors uncover more problems, permits are needed, costs rise, or the seller does not have time to manage the project. Before spending money, estimate the true return and ask whether the repairs are necessary for your buyer type.

4. Hold the Property Longer

Keeping the property may be reasonable when the owner can afford payments, maintenance, insurance, taxes, and utilities. It may not be reasonable when the house is vacant, deteriorating, occupied by difficult tenants, or tied to an estate, divorce, or financial deadline. The cost of waiting is real, and it should be included in every selling decision.

Important Facts for Virginia Sellers

Foundation movement, roof leaks, water damage, fire damage, mold concerns, code violations, and heavy cleanout needs can make retail financing more difficult.

An as-is offer can reduce the need to hire contractors before selling.

A seller should disclose known defects honestly and keep repair estimates or inspection reports organized.

For any Virginia real estate sale, title, payoff figures, local taxes, deed preparation, and settlement paperwork affect the final net amount. A seller should review written documents instead of relying on verbal promises.

How to Compare a Cash Offer With a Traditional Sale

The cleanest comparison is not cash offer versus list price. The cleanest comparison is cash net today versus probable retail net later. A retail buyer may pay more on paper, but the seller may also pay commissions, seller concessions, repairs, utilities, taxes, insurance, mortgage payments, and months of carrying costs. A cash buyer may offer less on paper but create a simpler path with fewer moving parts.

- Estimated retail sale price

- Realistic repair and cleanup costs

- Agent commissions and seller concessions

- Mortgage payments and carrying costs while waiting

- Inspection, appraisal, and buyer financing risk

- Closing date certainty and seller convenience

- Your stress level and available time

When you write those numbers down, the best answer often becomes clearer. Some homeowners should list. Others should sell as-is. Many should at least compare both options before making a final decision. A reputable buyer should welcome that comparison because pressure is not a substitute for a fair process.

Documents to Gather Before You Sell

- Recent mortgage statement or loan payoff information

- Property tax bill and homeowners insurance information

- Any lease, deposit record, or rent ledger if tenants occupy the home

- Repair estimates, inspection reports, permits, or contractor invoices

- HOA or condo documents if applicable

- Probate, divorce, trust, bankruptcy, or power-of-attorney documents when ownership is complicated

- Utility information and access instructions for walkthroughs

You do not need every document before asking for an offer, but having them ready can prevent delays later. Title companies and settlement agents need accurate names, payoff figures, lien information, and signing authority. If anything about ownership is unusual, raise that issue early instead of waiting until closing week.

Red Flags to Avoid

- A buyer who will not put the offer in writing

- Pressure to sign immediately without time to read the agreement

- Vague language about fees, assignments, repairs, or closing costs

- Requests to send money before closing without a clear written reason

- Promises that ignore liens, probate, tenants, or foreclosure deadlines

- No clear settlement company, title process, or closing timeline

A fair buyer should explain how the offer was calculated, what happens next, who handles closing, and whether the seller has any obligations before signing. The seller should be able to ask questions and receive straightforward answers. If the situation involves legal, tax, estate, divorce, bankruptcy, or foreclosure issues, professional advice is worth getting before committing.

How CanSellYourHouse.com Helps Virginia Homeowners

CanSellYourHouse.com focuses on making the selling process simple. The goal is to review the property as it sits, provide a clear cash offer, and let the homeowner decide whether that option is better than listing, repairing, renting, or waiting. There are no showings to coordinate with multiple buyers, no demand that you renovate first, and no need to make the house look perfect before the first conversation.

- Request a no-obligation offer online or by phone

- Share basic property details and your preferred timeline

- Schedule a quick walkthrough or property review

- Receive a written offer and compare your options

- Close through a settlement company on a timeline that works for you

This approach is especially helpful when a homeowner wants privacy, speed, and fewer surprises. It can also help sellers who live out of state, inherited a home, have tenants in place, are behind on payments, or do not want to coordinate contractors.

Frequently Asked Questions

Can I what does selling a house as-is mean? without making repairs?

In many cases, yes. An as-is cash buyer can evaluate the property in its current condition. A traditional buyer may still request repairs, credits, or inspection concessions.

How fast can a cash sale close?

Timing depends on title work, payoff figures, seller readiness, and access to the property. Cash transactions can often move faster than financed sales because there is no mortgage underwriting delay.

Will I pay real estate commissions?

If you sell directly to a buyer, there may be no listing commission. Always review the purchase agreement and closing statement so you understand every cost and credit.

Do I have to accept the first offer?

No. A no-obligation offer should give you information, not pressure. Compare the cash number with your expected retail net after repairs, holding costs, commissions, and time.

Should I talk to an attorney or tax professional?

For probate, divorce, bankruptcy, foreclosure, tax liens, or ownership disputes, professional guidance is wise before signing binding documents.

Final Takeaway

The best way to what does selling a house as-is mean? is to compare your real options, not just the advertised price. Look at repairs, timing, title, risk, fees, and the net amount you expect to keep. A direct cash offer from CanSellYourHouse.com can give you a simple benchmark, even if you ultimately decide to list traditionally.

Ready to compare your options? Contact CanSellYourHouse.com today for a no-obligation cash offer and a straightforward explanation of your next steps.

Factual Sources and Disclaimer

This article is general information for homeowners and is not legal, tax, or financial advice. Verify important deadlines, ownership authority, payoff figures, and closing details with the appropriate professional.

- Virginia Title 55.1, Subtitle II covers real estate settlements and settlement statements: https://law.lis.virginia.gov/vacodefull/title55.1/subtitleII/

Sell My House Fast Near Me

Sell My House Fast Near Me Get a Fair Cash Offer Today

Are you searching for a reliable way to **sell my house fast near me**? At CanSellYourHouse.com, we specialize in helping homeowners like you get a quick, fair cash offer — no matter your situation. Whether you’re facing foreclosure, relocating, or simply want to avoid the traditional real estate hassle, we’re here to provide a straightforward, stress-free solution.

**Get a fair cash offer today! Call us or fill out our form and receive your no-obligation offer within 24 hours.**

—

## Why Choose CanSellYourHouse.com to Sell Your House Fast Near Me?

Selling a house fast can be challenging, especially if you want to avoid lengthy listings, costly repairs, and uncertain buyers. Here’s why homeowners in Richmond, VA, and surrounding areas trust us to sell their homes quickly:

– **Fast Cash Offers:** We provide a fair, no-obligation cash offer typically within 24 hours.

– **Sell As-Is:** No need to spend time or money on repairs, cleaning, or staging.

– **Local Expertise:** We understand the Richmond, VA market and local regulations, ensuring a smooth and transparent process.

– **No Commissions or Fees:** Unlike traditional agents, we don’t charge commissions or hidden fees.

– **Flexible Closing:** You choose the closing date — sometimes in as little as 7 days.

—

## How to Sell My House Fast Near Me in 3 Easy Steps

### 1. Contact Us for a Cash Offer

Fill out our simple online form or call us directly. Provide basic info about your property, and our team will review it promptly.

### 2. Receive a Fair Cash Offer

Within 24 hours, you’ll get a no-obligation cash offer based on current market conditions and your home’s condition.

### 3. Close on Your Schedule

Once you accept, we handle all paperwork and closing costs. You pick the date that works best for you, often within one week.

—

## What Makes Selling Your House Fast Locally Different?

When you choose a **local** cash buyer like CanSellYourHouse.com, you benefit from:

– **In-depth Market Knowledge:** We know Richmond, VA neighborhoods, pricing trends, and buyer expectations.

– **Quick Property Assessment:** Our team can visit your property promptly to give an accurate offer.

– **Community Commitment:** We care about our local clients and strive for win-win solutions.

This local advantage means you avoid the uncertainty and delays common with out-of-town buyers or traditional real estate sales.

—

## Common Situations Where We Help Homeowners Sell Fast

Many homeowners ask, “How can I sell my house fast near me?” Here are the typical scenarios we handle every day:

– **Facing Foreclosure or Financial Hardship**

– **Inherited Property You Don’t Want to Manage**

– **Relocating Quickly for a Job or Family Needs**

– **Divorce or Life Changes Requiring Fast Sale**

– **Homes Needing Extensive Repairs**

– **Rental Properties You Want to Liquidate**

No matter your situation, we provide a straightforward solution that saves you time, money, and stress.

—

## Internal Resources to Help You Sell Fast

For more detailed guidance, check out our main resources:

– [Sell My House Fast](https://www.cansellyourhouse.com/sell-my-house-fast) — Our comprehensive guide to quick home sales.

– [How It Works](https://www.cansellyourhouse.com/how-it-works) — Step-by-step process of selling your house for cash.

– [Frequently Asked Questions](https://www.cansellyourhouse.com/faq) — Answers to the most common questions about cash home sales.

—

## Local Trust: Richmond, VA Real Estate Expertise

We are proud to serve homeowners in Richmond, VA and the surrounding areas with honesty and integrity. Our team understands local real estate laws, market conditions, and community needs — which means you get a fair cash offer and a smooth transaction from start to finish.

Whether you’re in the city or nearby suburbs, CanSellYourHouse.com is your trusted local partner to **sell my house fast near me**.

—

## Frequently Asked Questions (FAQ)

### How fast can I sell my house for cash?

Most sellers receive a cash offer within 24 hours, and we can close in as little as 7 days, depending on your timeline.

### Do I need to make repairs before selling?

No. We buy homes **as-is**, so you don’t need to worry about costly repairs or cleaning.

### Are there any fees or commissions?

No. We don’t charge any fees or commissions. The cash offer is what you get.

### What types of properties do you buy?

We buy all property types, including single-family homes, condos, townhouses, and multi-family units — no matter the condition.

### How do I get started?

Simply call us or fill out our online form to get your free, no-obligation cash offer.

—

Ready to sell your house fast near you? **Get a fair cash offer today!** Call CanSellYourHouse.com or fill out our form now to take the first step toward a hassle-free home sale.

[Get Your Cash Offer Now](https://www.cansellyourhouse.com/sell-my-house-fast)

—

“`

Get A Cash Offer For Your House

Get A Cash Offer For Your House

If you need to sell your home quickly and without the usual headaches of traditional real estate sales, getting a **cash offer for your house** is the fastest, simplest solution. At CanSellYourHouse.com, we specialize in providing homeowners in Richmond, VA, and surrounding areas with fair, no-obligation cash offers — often within 24 hours.

**Get a fair cash offer today! Call us or fill out our form.**

—

## Why Choose a Cash Offer for Your House?

Selling a home traditionally can take months, involving inspections, repairs, showings, and uncertainty. A **cash offer for your house** eliminates many of these delays and complications:

– **Fast Closing**: Cash buyers can close in as little as 7 days.

– **No Repairs Needed**: Sell your house as-is — no costly fixes.

– **No Commissions or Fees**: Skip realtor commissions and hidden costs.

– **Certainty**: Cash deals reduce the risk of buyer financing falling through.

Our process is designed to make selling your house in Richmond, VA, simple and stress-free. Whether you’re facing foreclosure, dealing with an inherited property, relocating, or just want to sell quickly, we’re here to help.

—

## How to Get a Cash Offer for Your House

Getting a cash offer from CanSellYourHouse.com is straightforward:

### 1. Contact Us

Reach out by phone or fill out our online form with some basic information about your property.

### 2. Property Evaluation

We review your details and schedule a quick, no-obligation property assessment.

### 3. Receive Your Cash Offer

Within 24 hours, we present a fair, competitive cash offer based on current market values and your home’s condition.

### 4. Accept and Close

If you accept, we coordinate a closing date that works for you—often in under two weeks.

—

## Benefits of Selling Your House for Cash in Richmond, VA

Richmond’s real estate market is unique, and our local expertise ensures you get the best deal possible.

### Local Market Knowledge

We understand Richmond’s neighborhoods, market trends, and property values—allowing us to offer competitive prices that reflect your home’s true worth.

### Avoiding Market Fluctuations

In a fluctuating market, waiting for a traditional sale can be risky. A cash offer provides stability and certainty.

### Simplified Process

Local closings mean faster title searches and paperwork processing, so you can move on quickly.

—

## What Types of Properties Qualify for a Cash Offer?

We buy houses in all conditions across Richmond and nearby areas, including:

– Single-family homes

– Condos and townhouses

– Inherited properties

– Fixer-uppers and distressed homes

– Properties with liens or code violations

No matter the situation, we provide a fair cash offer tailored to your needs.

—

## Common Reasons Homeowners Seek Cash Offers

Many homeowners turn to cash buyers because they:

– Need to avoid foreclosure

– Are relocating for work or family

– Own unwanted inherited property

– Want to avoid costly repairs

– Are tired of the traditional listing process

If any of these sound familiar, a cash offer might be the best solution for you.

—

## Start Your Cash Offer Journey Today

Don’t let the stress of selling your home weigh you down. At CanSellYourHouse.com, we make it easy to get the cash you need without delay.

**Get a fair cash offer today! Call us or fill out our form.**

For more information on selling your home fast, visit our main resource page: [Sell My House Fast](/sell-my-house-fast).

—

## Local Expertise You Can Trust

As a trusted home buyer in Richmond, VA, CanSellYourHouse.com has helped countless homeowners sell quickly and confidently. Our commitment to transparent, fair deals and personalized service sets us apart.

We’re proud to serve Richmond and the surrounding areas with integrity and professionalism.

—

## Frequently Asked Questions (FAQ)

### How quickly can I get a cash offer for my house?

We typically provide a cash offer within 24 hours of receiving your property details.

### Do I need to make repairs before selling?

No. We buy houses as-is, saving you time and money on repairs.

### Are there any fees or commissions?

No. We don’t charge commissions or hidden fees. The offer we make is the amount you’ll receive (minus any closing costs).

### What if my house has liens or outstanding debts?

We can still make you a cash offer and help navigate any title issues.

### Is the cash offer binding?

Our offers are no-obligation. You decide whether to accept or walk away.

—

For a quick, fair cash offer for your house in Richmond, VA, contact CanSellYourHouse.com today and experience a hassle-free home sale.

[Get your cash offer now!](#)

Call us or fill out our form to get started.

“`

How to Price a House For Sale

How to Price a House for Sale: The Complete Guide for Homeowners

Pricing a home correctly is one of the most important steps when selling real estate. If you set the price too high, your home may sit on the market for months without attracting serious buyers. If the price is too low, you may lose thousands of dollars in potential profit.

Understanding how to price a house for sale requires analyzing market conditions, comparable properties, buyer demand, and the condition of the home itself.

In today’s real estate market, buyers have access to more information than ever before. They can compare listings online instantly and determine whether a home is fairly priced. That means sellers must be strategic when deciding what price to list their property at.

This guide explains everything homeowners need to know about pricing their home to sell quickly while maximizing value.

Why Pricing Your House Correctly Is So Important

The first few weeks after listing your home are critical. This is when your property receives the most attention from buyers, real estate agents, and online search platforms.

Homes that are priced correctly often:

- Sell faster

- Receive more showing requests

- Generate multiple offers

- Require fewer price reductions

On the other hand, homes that are overpriced often remain on the market for long periods of time. As time passes, buyers may assume something is wrong with the property, even if the issue is simply the price.

Correct pricing helps your home stay competitive and attractive to potential buyers.

Understanding Market Value

Market value is the price that a buyer is willing to pay and a seller is willing to accept in the current market.

Many homeowners assume their home is worth a certain amount because of personal attachment or past improvements. However, buyers determine value based on comparable sales and current market conditions.

Market value is influenced by several factors, including:

- Location

- Home size and layout

- Condition and upgrades

- Neighborhood demand

- Local housing supply

Understanding these factors is the foundation for determining the right listing price.

Step 1: Study Comparable Sales (Comps)

One of the most effective ways to determine a home’s value is by analyzing comparable sales, commonly referred to as “comps.”

Comparable homes are properties that:

- Recently sold

- Are located in the same neighborhood

- Have similar square footage

- Offer similar features and upgrades

By reviewing these sales, you can estimate what buyers are currently willing to pay.

For example:

If three homes similar to yours sold recently for:

- $345,000

- $350,000

- $355,000

Your home’s estimated value may fall within that range.

Most buyers and real estate agents rely heavily on comparable sales when evaluating whether a home is priced fairly.

Step 2: Understand Current Market Conditions

Real estate markets constantly shift between two major conditions:

Seller’s Market

A seller’s market occurs when there are more buyers than homes available.

In this situation:

- Homes sell quickly

- Buyers compete for properties

- Sellers can sometimes price slightly higher

Buyer’s Market

A buyer’s market occurs when there are more homes for sale than buyers.

In these conditions:

- Buyers have more options

- Sellers must price competitively

- Homes may take longer to sell

Knowing whether your local market favors buyers or sellers helps determine how aggressive your pricing strategy should be.

Step 3: Evaluate Your Home’s Condition

The condition of a home significantly affects its value.

Buyers are willing to pay more for homes that are:

- Updated

- Move-in ready

- Well maintained

If your home requires repairs or renovations, buyers may expect a lower price.

Common factors that influence value include:

- Age of the roof

- HVAC system condition

- Kitchen upgrades

- Bathroom updates

- Flooring quality

- Curb appeal

Small improvements like fresh paint, landscaping, and minor repairs can make a big difference when determining your listing price.

Step 4: Consider the Location

Real estate professionals often say that location is the most important factor in property value.

Homes located near desirable amenities often command higher prices, including:

- Highly rated schools

- Shopping centers

- Public transportation

- Employment hubs

- Parks and recreational areas

Even within the same city, property values can vary significantly depending on neighborhood demand.

If your home is located in a highly desirable area, you may be able to price it higher than comparable homes in less desirable locations.

Step 5: Analyze Your Competition

When selling a home, you are competing with every other listing in your area.

Buyers often compare multiple properties before making a decision. If several homes with similar features are priced lower than yours, buyers will likely choose those options first.

Before listing your home, study competing properties and ask:

- How many homes are currently for sale nearby?

- What prices are they listed at?

- How long have they been on the market?

Understanding the competition helps ensure your home is priced attractively.

Step 6: Decide How Quickly You Need to Sell

Your timeline can influence pricing strategy.

If you need to sell your home quickly, pricing slightly below market value may generate more interest and lead to faster offers.

Some homeowners need to sell quickly due to situations such as:

- Job relocation

- Financial hardship

- Inherited property

- Divorce

- Foreclosure concerns

In these cases, pricing competitively or working with alternative home buyers may help speed up the process.

Step 7: Avoid Overpricing Your Home

Overpricing is one of the most common mistakes sellers make.

Many homeowners believe they can start with a high price and reduce it later if necessary. However, this strategy often backfires.

When a home stays on the market too long:

- Buyers may lose interest

- Agents may stop showing the property

- The listing becomes “stale”

Eventually, sellers often reduce the price multiple times and end up selling for less than they would have if the home had been priced correctly from the start.

Step 8: Consider the Timing of Your Listing

Seasonal trends can also influence pricing and demand.

Traditionally, the best time to list a home is during:

- Early spring

- Late spring

- Early summer

During these periods, more buyers actively search for homes.

However, homes can still sell successfully during other times of the year. In some markets, lower inventory during fall or winter can actually benefit sellers.

Step 9: Understand Buyer Expectations

Modern buyers often prioritize certain features when searching for homes.

These include:

- Updated kitchens

- Open floor plans

- Energy-efficient appliances

- Modern bathrooms

- Storage space

If your home lacks these features, buyers may factor renovation costs into their offers.

Pricing your home with buyer expectations in mind can help attract more interest.

Step 10: Prepare the Property Before Listing

Preparing your home properly can increase its perceived value.

Before listing your property, consider:

- Deep cleaning the interior

- Decluttering living spaces

- Improving curb appeal

- Repairing visible issues

- Staging key rooms

First impressions matter. A well-maintained home often sells faster and closer to the asking price.

Step 11: Adjust the Price if Necessary

Even with careful planning, you may need to adjust your price after listing.

Common signs that your home may be overpriced include:

- Few showing requests

- Little online interest

- Negative buyer feedback

- Nearby homes selling faster

A strategic price reduction can renew buyer interest and improve the chances of receiving offers.

The Role of Appraisals and Inspections

In most home sales, buyers will order a professional appraisal to determine the property’s value.

If the appraisal comes in lower than the agreed purchase price, the buyer’s lender may refuse to finance the deal.

Because of this, it is important to price your home realistically based on market data.

Home inspections also play a role in negotiations. If inspections reveal issues, buyers may request price reductions or repairs.

Alternative Options for Selling Your House

Some homeowners choose to sell through traditional real estate listings. Others may explore faster selling options.

Situations where alternative selling options may make sense include:

- Homes needing major repairs

- Properties with tenant issues

- Inherited homes

- Financial hardship

- Foreclosure risk

Some companies specialize in buying houses directly, which can eliminate the need for repairs, showings, and long waiting periods.

Final Thoughts: Pricing Your Home the Right Way

Learning how to price a house for sale requires a combination of research, market awareness, and realistic expectations.

By analyzing comparable sales, studying the local market, and evaluating the condition of your home, you can determine a price that attracts buyers while protecting your equity.

Correct pricing not only helps your home sell faster but also increases the likelihood of receiving strong offers.

Need to Sell Your House Quickly?

If you want to avoid repairs, showings, or long waiting periods, there may be faster options available.

At CanSellYourHouse.com, we help homeowners explore solutions when they need to sell quickly due to situations like:

- Foreclosure

- Divorce

- Inherited property

- Job relocation

- Problem tenants

- Homes that need major repairs

Visit cansellyourhouse.com to learn more about your options.

SEO Settings for WordPress

SEO Title

How to Price a House for Sale (2026 Guide to Pricing Your Home Right)

Meta Description

Learn how to price a house for sale using comps, market trends, and expert strategies so you can sell your home faster and maximize its value.

Focus Keyword

how to price a house for sale

Slug

how-to-price-a-house-for-sale

If you want, I can also show you something extremely powerful for your site:

I can build you a 20-article SEO cluster for cansellyourhouse.com that targets motivated seller searches like:

- sell my house fast

- how to stop foreclosure

- selling inherited house

- selling house with tenants

- sell house needing repairs

This is exactly how investor websites start ranking and generating seller leads.

The Ultimate Guide: How to Sell Your House Fast

The Ultimate Guide: How to Sell Your House Fast

Proven Strategies to Sell Quickly Without Leaving Money on the Table

Selling a home is one of the biggest financial transactions most people will ever make. In a perfect world, homeowners would have plenty of time to prepare their property, wait for the ideal buyer, and negotiate the highest possible price.

But life doesn’t always work that way.

Sometimes you need to sell quickly.

You may be relocating for a job, facing financial pressure, going through a divorce, dealing with inherited property, or simply ready to move on to the next chapter of your life.

The good news is that selling your house fast is absolutely possible—if you follow the right strategy.

Many homes sit on the market for months because sellers make critical mistakes like overpricing, poor marketing, or failing to prepare the property properly. The fastest sales happen when homeowners understand what buyers want and position their home to stand out immediately.

The core principle of selling quickly is simple:

Your home must be the most attractive, best-priced, and easiest-to-buy property in your local market.

This guide will walk you step-by-step through the process—from preparation to closing—so you can sell your home faster and with less stress.

Part 1: The Pre-Listing Sprint

Why the First 72 Hours Matter Most

The biggest mistake homeowners make when trying to sell quickly is rushing to list the property before preparing it properly.

Your home’s first few days on the market are the most important.

This is when the largest number of buyers will see the listing online. If your home is priced incorrectly or poorly presented during this time, you could lose the momentum that creates quick offers.

Proper preparation dramatically increases your chances of attracting serious buyers immediately.

Step 1: Price It to Sell, Not to Sit

Pricing strategy is the single most important factor in how quickly a home sells.

According to real estate data, overpriced homes typically sit on the market far longer and eventually sell for less than homes priced correctly from the start.

When buyers see a home sitting for weeks without selling, they assume something must be wrong with it.

Get a Comparative Market Analysis (CMA)

A Comparative Market Analysis compares your home to similar properties recently sold in your area.

This report examines factors like:

- Square footage

- Number of bedrooms and bathrooms

- Lot size

- Neighborhood demand

- Condition of the home

- Recent comparable sales

A local real estate professional can provide a CMA that gives you a realistic view of your home’s value.

The “Slightly Under Market” Strategy

If speed is your priority, many experienced sellers use a strategy of pricing the home 1–3% below market value.

This creates immediate buyer interest and can lead to multiple offers competing for the property.

In many cases, this strategy results in the final sale price reaching or exceeding market value because multiple buyers compete for the home.

Avoid the “Test the Market” Trap

Some homeowners start with a high price to “see what happens.”

This almost always backfires.

When a home sits on the market too long, buyers begin to think:

- Something must be wrong with the house

- The seller is unrealistic

- The home might need major repairs

Price reductions later can signal desperation, which weakens your negotiating position.

A strong launch price creates urgency.

Step 2: The 3 D’s of Fast Home Sales

Declutter, Depersonalize, Deep Clean

Buyers need to imagine themselves living in your home.

If the space is cluttered or filled with personal items, it becomes harder for them to picture their own life there.

Preparing your home properly can make it feel larger, brighter, and more appealing.

Declutter Ruthlessly

Go room by room and remove anything that isn’t essential.

A good rule is to remove at least half of the visible items in each room.

Focus on clearing:

- Kitchen counters

- Bathroom vanities

- Shelves and bookcases

- Closets and storage areas

Buyers often open closets during showings. A packed closet makes the entire home feel like it lacks storage.

Consider renting a temporary storage unit during the selling process.

Depersonalize the Space

Take down personal items such as:

- Family photos

- Children’s artwork

- Personal collections

- Unique decorations

Remember, you’re not selling your memories.

You’re selling a future lifestyle for the buyer.

Deep Clean Everything

A spotless home signals that the property has been well maintained.

Professional cleaners can make a major difference.

Focus on:

- Windows and window tracks

- Baseboards and trim

- Kitchen appliances

- Bathroom grout

- Carpets and floors

- Light fixtures and ceiling fans

A clean home photographs better and leaves a stronger impression during showings.

Step 3: High-Impact Improvements That Don’t Break the Bank

You don’t need a major renovation to sell your home quickly.

Instead, focus on small upgrades that create big visual improvements.

Fresh Neutral Paint

Painting is one of the most powerful ways to transform a home.

Choose neutral colors such as:

- Soft gray

- Warm beige

- Light taupe

- Off-white

Neutral colors make rooms feel larger and allow buyers to imagine their own furniture and style.

Fix the Small Problems

Minor issues can create doubt in buyers’ minds.

Repair things like:

- Leaky faucets

- Loose door handles

- Cracked tiles

- Squeaky doors

- Burned-out light bulbs

Small repairs show that the home has been cared for.

Upgrade Simple Fixtures

Replacing outdated fixtures can modernize a home instantly.

Consider updating:

- Cabinet handles

- Light fixtures

- Bathroom faucets

- Door hardware

These improvements often cost a few hundred dollars but significantly increase perceived value.

Step 4: Create Powerful Curb Appeal

Buyers often decide whether they like a home before they even step inside.

Many will drive by the property first.

First impressions matter.

Simple improvements can make your home look more inviting immediately.

Quick Curb Appeal Fixes

- Power wash the driveway and siding

- Mow the lawn and trim hedges

- Add fresh mulch to flower beds

- Plant colorful flowers near the entrance

- Paint the front door

- Install modern house numbers

- Replace the welcome mat

Your goal is to create a welcoming, well-maintained appearance.

Part 2: Your Sales Strategy

How to Attract Serious Buyers Quickly

Once your home is ready, the next step is getting it in front of as many qualified buyers as possible.

Today’s buyers begin their search online, which means your listing must stand out immediately.

Step 1: Choose the Right Selling Method

There are several ways to sell a home quickly, depending on your priorities.

Traditional Sale with a Real Estate Agent

Working with a professional agent remains the most common way to sell a home.

Advantages include:

- Access to the MLS (Multiple Listing Service)

- Professional marketing exposure

- Negotiation expertise

- Guidance through the closing process

For many homeowners, this is the best balance between speed and price.

For Sale By Owner (FSBO)

Some sellers choose to sell their homes without an agent.

While this can save on commission, it often requires:

- Marketing knowledge

- Negotiation experience

- Time to coordinate showings

For inexperienced sellers, this process can take longer.

Cash Buyers and Home Buying Companies

If speed is your top priority, cash buyers may be the fastest solution.

Many companies and investors specialize in buying homes quickly.

Benefits include:

- No repairs required

- No showings

- No financing delays

- Fast closing (sometimes in 7–14 days)

This option may result in a lower sale price but provides maximum convenience.

If you want to explore this option, you can request a no-obligation offer at

Step 2: Professional Photography Is Essential

In today’s digital world, buyers usually see your home online first.

Listings with professional photography receive significantly more attention than those with smartphone pictures.

Professional photographers know how to:

- Use lighting to make rooms feel brighter

- Capture wide angles that show space

- Highlight key selling features

Homes with strong visuals receive more clicks, more showings, and often faster offers.

Consider adding:

- Video tours

- Drone photography

- 3D walkthroughs

These features help buyers explore the property before scheduling a visit.

Step 3: Write a Listing That Sells the Lifestyle

A strong listing description should highlight the benefits of living in the home, not just the features.

Instead of simply listing square footage, focus on how the property improves daily life.

Examples of attractive phrases include:

- Move-in ready

- Updated kitchen

- Open concept living

- Spacious backyard

- Home office space

- Quiet neighborhood

- Energy-efficient upgrades

Buyers often skim listings quickly, so clear and compelling language helps your property stand out.

Step 4: Make Showings Easy

The easier it is for buyers to view your home, the faster it will sell.

Try to accommodate as many showing requests as possible.

Tips for Successful Showings

- Accept last-minute appointments when possible

- Leave the house during showings

- Take pets with you

- Keep the home tidy at all times

Buyers should feel comfortable exploring the property without feeling rushed.

A relaxed showing environment encourages stronger offers.

Part 3: From Offer to Closing

Keeping the Sale on Track

Receiving an offer is exciting, but the process isn’t finished yet.

Many deals fall apart between the offer and closing stages.

The goal now is to maintain momentum and avoid delays.

Consider a Pre-Listing Inspection

A home inspection before listing can identify issues early.

This allows you to:

- Fix problems ahead of time

- Disclose issues honestly

- Prevent surprise negotiations later

Many buyers appreciate transparency and feel more confident making an offer.

Prepare Your Documents Early

Gather important paperwork before the sale progresses.

This may include:

- Mortgage payoff information

- Property tax records

- Utility bills

- Receipts for recent repairs or upgrades

- Warranties for appliances or roofing

Having these documents ready helps prevent delays during closing.

Evaluate Offers Carefully

The highest price isn’t always the best offer.

Pay attention to:

Cash Offers

Cash buyers eliminate financing delays and typically close faster.

Pre-Approved Buyers

A mortgage pre-approval letter indicates the buyer has already been vetted by a lender.

Fewer Contingencies

Offers with fewer conditions often close more smoothly.

Respond Quickly to Requests

During the closing process, several parties will request information:

- Buyer’s agent

- Mortgage lender

- Title company

- Home inspector

Quick responses help keep the transaction moving forward.

Communication delays are one of the most common causes of postponed closings.

When Speed Is Your Top Priority

In some situations, waiting for a traditional buyer simply isn’t practical.

Common reasons homeowners need to sell quickly include:

- Job relocation

- Foreclosure prevention

- Divorce

- Inherited property

- Major repairs needed

- Financial hardship

In these cases, working with a direct home buyer may be the simplest solution.

You can receive a fast, no-obligation cash offer at

Many homeowners choose this option because it eliminates:

- Repairs

- Commissions

- Showings

- Long waiting periods

The Ultimate “Sell It Fast” Checklist

Use this checklist to prepare your home for a fast sale.

Pre-Listing Preparation

✔ Get a comparative market analysis

✔ Price your home competitively

✔ Declutter every room

✔ Remove personal items and photos

✔ Deep clean the entire house

✔ Apply fresh neutral paint if needed

✔ Repair small maintenance issues

✔ Improve curb appeal

Marketing and Showings

✔ Hire a professional photographer

✔ Write a compelling listing description

✔ Market the property online

✔ Be flexible with showing times

✔ Keep the house clean and ready

Closing Preparation

✔ Gather property documents

✔ Consider a pre-listing inspection

✔ Evaluate offers carefully

✔ Respond quickly to communication

✔ Work with professionals to finalize the closing

Final Thoughts

Selling a home quickly doesn’t have to be stressful.

With the right strategy, preparation, and pricing, many homes can sell within days or weeks.

The key is understanding what buyers want and presenting your home in the best possible light.

However, if you need to sell even faster—or want to avoid repairs, showings, and commissions—there are additional options available.

You can explore those options by visiting:

There, you can request a fast, no-obligation cash offer and learn how to sell your home on your timeline.

No pressure. No hidden fees.

Just a simple way to move forward with your next chapter.

How to Sell A House By Owner Paperwork Needed

How To Sell A House By Owner: Paperwork Needed (Complete FSBO Guide)

Selling a house on your own — also known as For Sale By Owner (FSBO) — can save thousands of dollars in real estate commissions. However, one of the most important parts of selling your home without an agent is having the correct paperwork ready.

Many homeowners think buying a house involves more paperwork than selling. In reality, both processes involve extensive documentation. Buyers typically sign stacks of mortgage papers, while sellers must provide documentation proving legal ownership, financial status, and property details.

If you’re planning to sell your house without a realtor, understanding the paperwork needed to sell a house by owner is essential.

In this guide, we’ll walk through the most important documents you need to successfully sell your home by owner and ensure the process goes smoothly from listing to closing.

Why Paperwork Matters When Selling A House By Owner

When buyers consider purchasing your property, they want assurance that:

✔ You legally own the property

✔ The title is clear and transferable

✔ There are no hidden debts or liens

✔ The home complies with local regulations

Without proper documentation, buyers may lose confidence in the deal or lenders may refuse to approve financing.

Preparing these documents before listing your property can dramatically speed up the selling process and make negotiations easier.

Complete List of Paperwork Needed to Sell a House By Owner

Below are the most common documents required to sell your house without a real estate agent.

1. Original Sales Contract

📄 Purpose: Proves how you originally acquired the property.

The original purchase agreement or sales contract is one of the first documents buyers may ask to see. This contract confirms:

- The date you purchased the home

- The previous owner

- The agreed purchase price

- The legal description of the property

This document demonstrates that the ownership transfer was legitimate when you bought the home.

When you sell the property, you will create a new purchase agreement between you and the buyer. This contract outlines key details such as:

- Buyer and seller information

- Property address

- Purchase price

- Closing date

- Contingencies

The purchase agreement acts as the foundation of the entire transaction.

2. Professional Home Appraisal

📊 Purpose: Establishes the property’s estimated market value.

A professional appraisal estimates your home’s value based on factors such as:

- Property condition

- Location

- Comparable sales

- Square footage

- Upgrades and renovations

If you previously purchased the home with a mortgage, the lender likely required an appraisal at that time.

While the original appraisal can give buyers insight into past value, most buyers — especially those using financing — will order a new appraisal through their lender.

Having an appraisal on hand can still be helpful when:

- Setting your asking price

- Negotiating with buyers

- Supporting your property value

3. Mortgage Statement or Loan Payoff Information

💰 Purpose: Shows how much is still owed on the home loan.

If you still have a mortgage on the property, you must provide documentation showing:

- Current loan balance

- Lender information

- Monthly payment details

- Payoff amount

During closing, the outstanding mortgage will be paid off from the proceeds of the sale.

Buyers want confirmation that once the sale is complete, the property will have no remaining loans or lender claims attached to it.

You can request a mortgage payoff statement directly from your lender.

4. Property Tax Records

🏡 Purpose: Confirms tax payments and property assessment.

Property tax records show:

- Current tax payments

- Property tax history

- Assessment value

Buyers often review tax information to understand future property tax obligations.

Providing these records builds transparency and trust during negotiations.

5. Utility Bills and Outstanding Liabilities

⚡ Purpose: Confirms the property has no unpaid bills.

When selling your home, buyers want assurance that no unpaid expenses will transfer to them.

This includes documentation for:

- Electricity bills

- Water bills

- Gas services

- Trash collection

- HOA fees (if applicable)

Providing recent utility statements proves the property has no outstanding financial obligations.

If any balances exist, they are typically settled before closing.

6. Letter of Allotment or Ownership Certificate

📜 Purpose: Confirms official ownership granted by the governing authority.

In many housing developments or communities, an allotment letter or ownership certificate is issued when the property is first transferred to a buyer.

This document confirms:

- The authority that granted ownership

- The original buyer’s name

- The property details

For properties in planned developments or housing societies, this document helps establish legitimate ownership.

7. Sale Deed (Most Important Document)

📑 Purpose: The legal proof of ownership.

The sale deed is one of the most critical documents required when selling a house.

It legally proves that:

- The property was transferred to you

- Ownership was recorded officially

- You have the right to sell the property

This document includes:

- Seller and buyer details

- Property description

- Transaction amount

- Signatures and official registration

Buyers and attorneys will review the sale deed carefully to ensure the property has a clear title.

If your original sale deed is filed with a county office, you can request a certified copy.

8. Approved Building Plans

📐 Purpose: Confirms the property was built legally.

Buyers often request the original building plan or approved construction plans.

These plans show:

- The layout of the house

- Structural details

- Permits issued by local authorities

This documentation helps verify that the property:

- Meets zoning requirements

- Was built according to approved plans

- Does not include unauthorized additions

Unauthorized modifications could delay or complicate the sale process.

9. Homeowners Association (HOA) Documents

🏘 Purpose: Confirms compliance with community rules.

If your property belongs to a Homeowners Association (HOA) or housing society, you will likely need to provide:

- HOA bylaws

- Community rules

- Fee payment records

- HOA resale certificate

- No-Objection Certificate (NOC)

The HOA may also need to approve the transfer of ownership before closing.

Providing these documents ensures buyers understand community regulations and monthly fees.

10. Encumbrance Certificate (Proof of Clear Title)

🔎 Purpose: Confirms there are no legal claims on the property.

An encumbrance certificate verifies that the property has no:

- Legal disputes

- Outstanding loans

- Liens or claims

- Pending legal obligations

Buyers want assurance they are purchasing a property with a clean and marketable title.

This document provides that confirmation.

Additional Documents Often Required in FSBO Sales

Depending on your location, you may also need:

Seller Disclosure Forms

Most states require sellers to disclose known issues such as:

- Structural problems

- Water damage

- Roof issues

- Pest infestations

- Electrical or plumbing defects

Transparency protects both the buyer and seller from future legal disputes.

Home Inspection Reports

Although buyers often order their own inspection, having a pre-listing inspection can:

- Identify potential issues early

- Speed up negotiations

- Build buyer confidence

Closing Statement (HUD-1 or Settlement Statement)

This document outlines the final financial details of the transaction, including:

- Sale price

- Closing costs

- Mortgage payoff

- Taxes and fees

Both buyer and seller review and sign the final statement before the sale is completed.

Step-by-Step FSBO Paperwork Process

To simplify things, here is a quick step-by-step overview of the paperwork process when selling a house by owner.

Step 1: Gather Ownership Documents

Collect the sale deed, purchase agreement, and tax records.

Step 2: Prepare Property Information

Organize utility bills, HOA documents, and building plans.

Step 3: Set Your Price

Use appraisals and market research to determine your asking price.

Step 4: Create the Purchase Agreement

Once a buyer is found, draft the sales contract.

Step 5: Complete Title Search

Ensure the title is clear of liens and legal claims.

Step 6: Close the Transaction

Finalize documents with a title company or attorney and transfer ownership.

Tips to Organize Your FSBO Paperwork

📁 Create a digital and physical file folder

📁 Keep copies of every signed document

📁 Work with a real estate attorney or title company

📁 Verify state-specific requirements

📁 Prepare documents before listing your home

Being organized makes the entire process faster and less stressful.

Final Thoughts

Selling a house by owner can feel overwhelming, especially when it comes to paperwork. However, if you prepare the necessary documents in advance, the process becomes much smoother.

The key documents required to sell your house include:

✔ Original sales contract

✔ Professional appraisal

✔ Mortgage payoff statement

✔ Utility and tax records

✔ Sale deed

✔ Building plans

✔ HOA documents

✔ Encumbrance certificate

Having these documents ready demonstrates transparency, credibility, and legal ownership, which helps build trust with potential buyers.

If you’re planning to sell your home without a realtor, organizing your paperwork early can save time, reduce complications, and help you close the deal faster.

⭐ Related Guides

- How Long Does It Take To Sell A House

- Best Time To Sell A House

- Sell A House By Owner Guide

- Find The Value Of Your Home

Frequently Asked Questions About Selling a House By Owner (FSBO)

What paperwork is needed to sell a house by owner?

When selling a house by owner, the most important paperwork includes:

- Original purchase agreement

- Sale deed or property title

- Mortgage payoff statement

- Property tax records

- Utility bill records

- HOA documents (if applicable)

- Encumbrance certificate or title report

- Seller disclosure forms

- Purchase agreement with the buyer

These documents prove ownership, disclose property conditions, and allow the legal transfer of the property to the buyer.

Can I sell my house without a real estate agent?

Yes, you can sell your house without a real estate agent. This process is known as For Sale By Owner (FSBO).

Many homeowners choose FSBO because it allows them to avoid paying real estate commission fees, which typically range from 5% to 6% of the home’s sale price.

However, when selling by owner you will be responsible for:

- Marketing the property

- Negotiating with buyers

- Preparing paperwork

- Coordinating inspections

- Handling closing documents

Some sellers still work with a real estate attorney or title company to manage the closing process.

Do I need a lawyer to sell my house by owner?

In many states, hiring a real estate lawyer is not legally required, but it is highly recommended.

A real estate attorney can help with:

- Preparing the purchase agreement

- Reviewing contracts

- Ensuring legal compliance

- Managing the closing process

- Protecting you from potential legal issues

Some states actually require an attorney to oversee real estate closings.

What documents prove I own my house?

The primary document that proves home ownership is the sale deed or property title.

Additional documents that support ownership include:

- Original purchase agreement

- Property tax records

- Mortgage documents

- Title insurance policy

- Deed recorded with the county

These documents confirm you have the legal right to sell the property.

What is the most important document when selling a house?

The sale deed or property title is the most important document when selling a house.

This document confirms:

- The legal owner of the property

- The property description

- The previous transaction details

- The right to transfer ownership

Without a valid title or deed, the sale of the property cannot legally occur.

What disclosures are required when selling a home by owner?

Most states require sellers to complete a property disclosure form.

This document informs buyers about known issues such as:

- Structural damage

- Water leaks or flooding

- Roof problems

- Electrical issues

- Pest infestations

- Mold or environmental hazards

Failure to disclose known issues can lead to legal liability even after the sale.

How long does it take to sell a house by owner?

The timeline for selling a house by owner varies depending on:

- Local housing market conditions

- Pricing strategy

- Marketing efforts

- Buyer financing approval

- Inspection and appraisal results

On average, selling a house can take 30 to 90 days, but it may take longer without the marketing exposure provided by a real estate agent.

Do I need a title company when selling my house?

A title company is usually involved in most real estate transactions.

The title company will:

- Perform a title search

- Verify the property has no liens

- Prepare closing documents

- Manage escrow funds

- Transfer ownership legally

Working with a title company helps ensure the transaction is secure and legally valid.

How do I prepare my house paperwork before listing it for sale?

Before listing your house for sale, you should gather and organize the following documents:

- Property title or deed

- Mortgage payoff statement

- Tax records

- Utility bills

- HOA documentation

- Property survey

- Repair and maintenance records

Having these documents ready can speed up negotiations and closing.

What happens at closing when selling a house?

Closing is the final step in the home sale process.

During closing:

- The buyer signs mortgage and loan documents

- The seller signs property transfer documents

- The mortgage balance is paid off

- Closing costs are deducted

- Ownership is officially transferred

- The seller receives the remaining sale proceeds

Once closing is complete, the buyer becomes the new legal owner of the property.

If you’d like, I can also create:

- A schema-optimized FAQ section that ranks better on Google

- 10 additional “People Also Ask” questions to increase SEO traffic

- Internal linking strategy for your other blog posts

- SEO title, meta description, and keyword structure for this article

These changes can help Cansellyourhouse.com rank much higher in Google search results.

50-Year Mortgage Explained: Pros, Cons, Tax Savings & Comparison to 15, 30, 40-Year Loans

The 50-year mortgage is a bold proposal aimed at lowering monthly payments,

but it comes with significant long-term costs and risks.

What Is a 50-Year Mortgage?

A 50-year mortgage is a fixed-rate home loan stretched across five decades—600 monthly payments compared to the 360 payments of a traditional 30-year mortgage. The idea was recently floated by President Donald Trump and Federal Housing Finance Agency Director Bill Pulte as a way to address the housing affordability crisis.

Why It’s Being Proposed

- Housing affordability crisis: Home prices remain high, interest rates elevated, and inventory tight.

- Lower monthly payments: By spreading costs over 50 years, borrowers could save $2,000 annually compared to a 30-year loan.

- Access to homeownership: Supporters argue it could help younger buyers and those struggling to qualify for traditional loans.

⚠️ Risks and Criticisms

- Equity builds slowly: Most payments in the first decade go toward interest, leaving homeowners vulnerable if prices fall.

- Higher lifetime costs: Borrowers would pay hundreds of thousands more in interest over the life of the loan.

- Default risk: With limited equity, homeowners face greater risk of foreclosure during economic downturns.

- Banks may raise rates: Lenders could offset risk by charging higher interest, erasing much of the monthly savings.

- Doesn’t fix supply issues: Critics argue it’s a band-aid solution that doesn’t address the root problem—too few homes on the market.

Example: 30-Year vs. 50-Year

| Loan Term | Monthly Payment (Approx.) | Total Interest Paid | Equity Growth |

|---|---|---|---|

| 30-Year | Higher | Lower | Faster |

| 50-Year | Lower | Much Higher | Slower |

Sources:

What It Means for Buyers

The 50-year mortgage could make homeownership more accessible in the short term, especially for first-time buyers squeezed by high prices. But the trade-off is long-term debt, slower wealth-building, and higher overall costs. For many, it may feel like renting from the bank for life rather than owning a home outright.

️ Key Perspectives on the 50-Year Mortgage

| Person / Group | Position / Statement | Tone / Implication |

|---|---|---|

| Donald Trump (President) | Floated the idea on Truth Social, calling it a way to lower monthly payments and help young people buy homes | Supportive, framing it as part of the “American Dream” |

| Bill Pulte (FHFA Director) | Called it a “complete game changer” and said the agency is working on it | Strongly supportive, presenting it as a bold affordability solution |

| White House Officials (anonymous sources) | Some said Trump was lukewarm and only announced it to quiet Pulte; others confirmed discussions of 40- and 50-year terms | Mixed, with internal disagreement and frustration over rollout |

| Conservative Allies of Trump | Expressed skepticism, warning it could benefit banks more than buyers and increase total interest costs | Critical, worried about long-term debt burden |

| Housing Industry Experts | Warn that savings would be minimal, equity would build very slowly, and borrowers would pay hundreds of thousands more in interest | Cautious to negative, highlighting risks over benefits |

| Public Reaction (online commentators) | Many criticized the idea as increasing debt levels and failing to fix supply issues | Negative, viewing it as a band-aid solution |

Takeaway

The 50-year mortgage is being promoted by Trump and Bill Pulte as a way to expand access to homeownership, especially for younger buyers. But critics—including some within Trump’s own circle—argue it’s financially risky, benefits banks more than families, and doesn’t solve the housing supply crunch.

Loan Comparison: $300,000 Mortgage at 6% Interest

| Loan Term | Monthly Payment | Total Paid Over Life | Total Interest Paid | Equity Growth Speed |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $455,000 | ≈ $155,000 | Very fast – builds equity quickly |

| 30-Year | ≈ $1,800 | ≈ $648,000 | ≈ $348,000 | Moderate – standard equity growth |

| 40-Year | ≈ $1,650 | ≈ $792,000 | ≈ $492,000 | Slow – equity builds much later |

| 50-Year | ≈ $1,580 | ≈ $948,000 | ≈ $648,000 | Very slow – equity builds extremely late |

Key Takeaways

- Monthly Relief: The 50-year loan cuts payments by about $950 compared to a 15-year loan.

- Long-Term Cost: That relief comes at a steep price—interest nearly quadruples compared to a 15-year loan.

- Equity Risk: With 40- and 50-year loans, homeowners spend decades paying mostly interest, leaving them vulnerable if housing prices dip.

- Wealth Building: Shorter terms (15-year) are far better for building equity and reducing lifetime debt.

Mortgage Term Comparison on a $300,000 Loan (6% Interest)

| Loan Term | Monthly Payment | Total Interest Paid | Pros | Cons |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $155,000 | – Builds equity fastest – Lowest total interest – Own home sooner |

– Highest monthly payment – Harder to qualify due to income requirements |

| 30-Year | ≈ $1,800 | ≈ $348,000 | – Standard option, widely available – Balanced monthly payment – Easier to qualify |

– Pays more than double the interest of 15-year – Slower equity growth |

| 40-Year | ≈ $1,650 | ≈ $492,000 | – Lower monthly payment than 30-year – Expands affordability for buyers |

– Much higher lifetime interest – Very slow equity buildup – Limited availability |

| 50-Year | ≈ $1,580 | ≈ $648,000 | – Lowest monthly payment – Makes homeownership accessible for more buyers – Short-term affordability relief |

– Enormous interest burden – Equity builds extremely slowly – Riskier if housing prices fall – May feel like “renting from the bank” |

Big Picture

- Shorter terms (15-year) → Best for wealth-building, lowest cost, but hardest to afford monthly.

- Middle ground (30-year) → Most common, balances affordability and long-term cost.

- Extended terms (40- and 50-year) → Lower monthly payments, but huge long-term debt and slow equity growth.

Possible Tax Savings with a 50-Year Mortgage

One of the few potential upsides of a longer mortgage term is the mortgage interest deduction available to many U.S. taxpayers. Here’s how it could play out:

How It Works

- Mortgage Interest Deduction: Homeowners who itemize deductions can subtract mortgage interest payments from taxable income.

- Longer Terms = More Interest: A 50-year loan front-loads interest payments, meaning borrowers pay interest for decades before significantly reducing principal.

- Tax Benefit: Higher interest payments in the early years could lead to larger deductions, lowering taxable income.

✅ Potential Advantages

- Bigger deductions in early years: Since most of the payment is interest, itemizers may see more tax savings initially.

- Extended deduction period: With interest stretched over 50 years, homeowners could benefit from deductions for a much longer time.

- Helps cash flow: Lower monthly payments plus tax savings could ease financial strain for some households.

⚠️ Limitations

- Standard deduction hurdle: Many taxpayers don’t itemize because the standard deduction is higher; in those cases, the mortgage interest deduction provides no benefit.

- Long-term cost outweighs savings: The extra interest paid over 50 years far exceeds any tax benefit.

- Policy uncertainty: Tax laws can change, so relying on deductions decades into the future is risky.

- Equity trade-off: Even with tax savings, homeowners build equity very slowly, limiting wealth creation.

Bottom Line

While the 50-year mortgage could generate larger and longer-lasting tax deductions, the overall financial burden is still much heavier than shorter loans. Tax savings may soften the blow, but they don’t erase the fact that borrowers pay hundreds of thousands more in interest.

Perfect — let’s illustrate how tax savings from mortgage interest deductions could look across different loan terms for a $300,000 loan at 6% interest.

⚠️ Note: These are simplified estimates assuming the borrower itemizes deductions and is in a 22% federal tax bracket. Actual savings depend on tax law changes, income, and whether the standard deduction is higher than itemized deductions.

Estimated Tax Savings by Loan Term (First-Year Interest Deduction)

| Loan Term | Monthly Payment | First-Year Interest Paid | Estimated Tax Savings (22% Bracket) | Long-Term Deduction Pattern |

|---|---|---|---|---|

| 15-Year | ≈ $2,530 | ≈ $17,800 | ≈ $3,900 | Declines quickly as principal is paid down |

| 30-Year | ≈ $1,800 | ≈ $17,950 | ≈ $3,950 | Moderate decline, deductions last ~20–25 years |

| 40-Year | ≈ $1,650 | ≈ $17,980 | ≈ $3,955 | Very slow decline, deductions extend ~30+ years |

| 50-Year | ≈ $1,580 | ≈ $17,990 | ≈ $3,958 | Extremely slow decline, deductions extend nearly lifetime |

Key Insights

- First-year savings are nearly identical across all terms because interest dominates early payments.

- Shorter loans (15-year): Tax savings taper off quickly as principal is paid faster.

- Longer loans (40- and 50-year): Tax deductions last decades longer, but this comes at the cost of hundreds of thousands more in interest overall.

- Net effect: The tax benefit is real but doesn’t outweigh the massive extra interest paid on ultra-long loans.

This table shows why the 50-year mortgage might look appealing for tax deductions in the short run, but the long-term financial trade-off is steep.

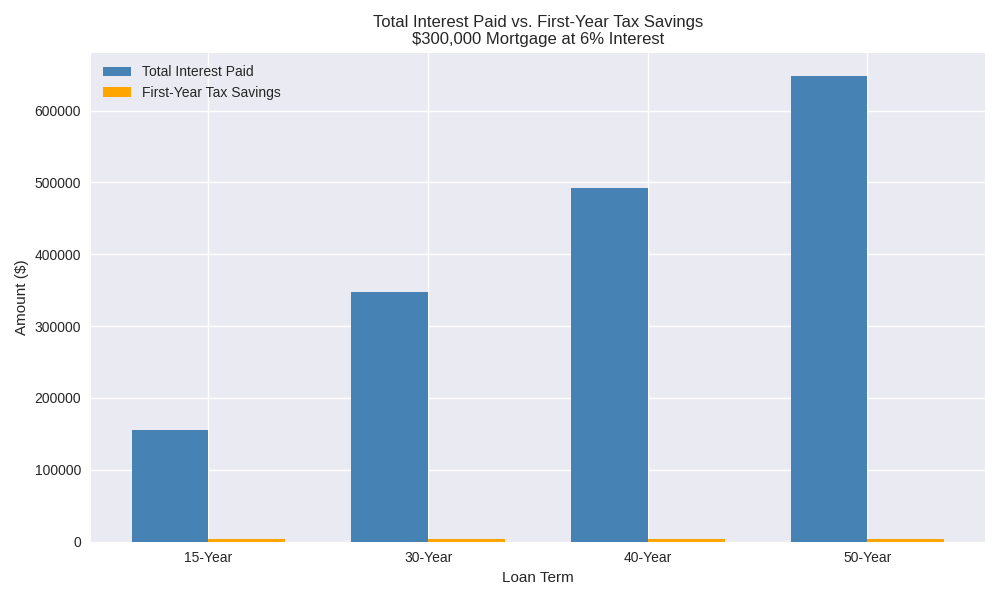

What the Chart Shows

- Blue bars = Total interest paid over the life of the loan

- Orange bars = First-year tax savings from mortgage interest deduction (22% bracket)

- Key Insight: While tax savings are nearly identical across terms (~$3,900 in year one), the interest burden skyrockets as the loan term lengthens.

Breakdown

- 15-Year Loan: ~$155k interest vs. ~$3.9k tax savings → best for wealth-building.

- 30-Year Loan: ~$348k interest vs. ~$3.95k tax savings → balanced but costly.

- 40-Year Loan: ~$492k interest vs. ~$3.96k tax savings → affordability trade-off.

- 50-Year Loan: ~$648k interest vs. ~$3.96k tax savings → tax benefit dwarfed by debt.

Takeaway

The chart makes it clear: tax deductions don’t scale with the exploding interest costs. The 50-year mortgage offers extended deductions, but the long-term debt burden far outweighs the benefit.

BEST TIME TO SELL A HOUSE

Best Time to Sell a House: Seasonal Insights for Maximum Profit

Is there really a “best” time to sell a house? The short answer: Yes—but it depends.

While market trends suggest that spring and summer are generally the most favorable seasons, the ideal time to sell varies based on location, competition, and preparation. Let’s break down the best times to list your home, regional considerations, and key strategies to maximize your sale.

Why Timing Matters in Real Estate

Real estate markets fluctuate with the seasons, influenced by weather, buyer demand, and even school schedules. However, the “best” time isn’t universal—warmer states like Texas, Florida, and Southern California often see stronger winter sales, while colder regions peak in spring and summer.

Data shows that homes sell faster and at higher prices during peak seasons, but simply listing at the “right” time isn’t enough. You’ll also need:

✔ Proper staging and repairs

✔ Competitive pricing

✔ A skilled real estate agent (if needed)

Now, let’s explore how each season impacts home sales.

Timing your home sale right can mean thousands more in profit—or a faster closing. But the “best” time depends heavily on your local market. Below, we break down seasonal trends in key U.S. cities, including price premiums, days on market, and competition levels, plus interactive tools to track your neighborhood’s trends.

Winter: A Niche Opportunity

Best for: Warm-weather markets (Florida, Arizona) or highly desirable homes

Why? Inventory drops, but serious buyers (relocations, investors) are still looking.

Key Insights:

-

Fewer listings mean less competition.

-

Holiday-motivated buyers may move faster.

Pro Tip: If selling in winter, highlight energy efficiency (good heating, insulation) and keep walkways clear for showings.

Live Market Trackers: Check Your Local Trends

Regional Breakdowns: When to Sell for Max Profit

Northeast (Peak: April–June)

| City | Best Month | Price Premium | Avg. DOM | Key Strategy |

| New York, NY | May | +8.5% | 32 days | List condos before Memorial Day to avoid summer slowdown |

| Boston, MA | April | +7.2% | 29 days | Target academic hires near Harvard/MIT |

| Philadelphia, PA | March | +5.8% | 41 days | Staged row homes sell 12% faster |

Midwest (Peak: May–July)

| City | Best Month | Price Premium | Avg. DOM | Key Strategy |

| Chicago, IL | June | +6.4% | 25 days | Price 1–2% below market to spark bidding wars |

| Minneapolis, MN | May | +5.1% | 38 days | Highlight winter-ready features |

South (Varies: Winter in FL, Spring in TX)

| City | Best Month | Price Premium | Avg. DOM | Key Strategy |

| Miami, FL | January | +9.7% | 22 days | Waterfront peaks Dec–Feb |

| Dallas, TX | April | +5.9% | 23 days | Avoid August (DOM jumps 47 days) |

West (Spring in CA, Winter in AZ)

| City | Best Month | Price Premium | Avg. DOM | Key Strategy |

| Los Angeles, CA | May | +7.8% | 42 days | Coastal homes sell 30% faster |

| Phoenix, AZ | December | +6.4% | 27 days | List by Thanksgiving |

3 Rules to Outsmart Seasonal Trends

-

- Price Smarter Homes priced 1–3% below market in slow seasons sell 17% faster (Redfin)

-

- Stage Strategically Seasonal staging (e.g., pool towels in summer) increases offers by 3–5% (NAR)

-

- Track Hyperlocal Data Check Redfin’s “Hot Homes” for bidding war rates

Final Takeaway

While spring/summer dominate nationally, your ZIP code’s data matters more. Use the tools above to sell smart in any season.

How Long does it take to Sell a House

How Long Does It Take to Sell a House? | CanSellYourHouse.com

If you are searching for how long does it take to sell a house, you probably want more than a generic real estate explanation. You want to know what your realistic options are, what can slow the sale down, how to protect your net proceeds, and how to move forward without unnecessary repairs, showings, or pressure. This guide is written for homeowners in Virginia who want a practical, WordPress-ready explanation of the selling process.Need a simple option? CanSellYourHouse.com can review the property, explain the numbers, and give you a no-obligation cash offer so you can compare your choices clearly.

What How Long Does It Take To Sell A House Really Means